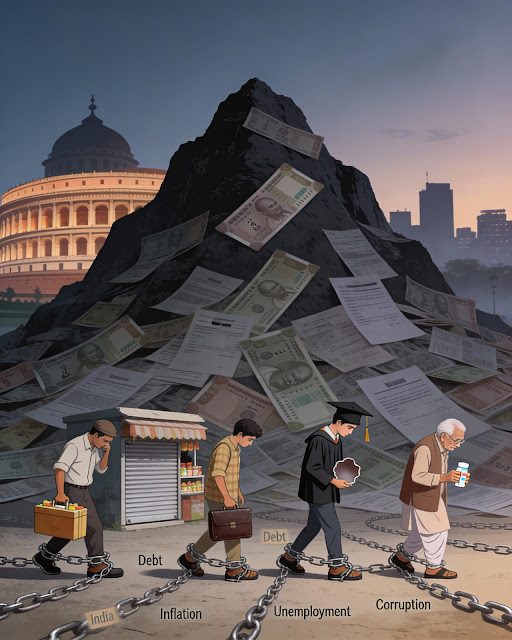

India in a Debt Trap: Every Citizen Owes About ₹1.5 Lakh

Rising prices and unemployment are no longer limited to markets. They are felt in every home, kitchen, and household budget. Government figures may show improvement, but the reality for ordinary people is very different. Daily essentials such as vegetables, cooking oil, rent, soap, and fuel have become more expensive, while people’s buying power has gone down.

In the last year, the price of an LPG gas cylinder increased sharply. A small relief before elections was later taken back with fresh price hikes. Today, a large part of a middle-class family’s income is spent just on cooking gas. When fuel prices rise, the cost of everything else also goes up. Despite government claims of price control and lower inflation, people do not see relief in local markets.

Big FMCG companies like Hindustan Unilever, ITC, Dabur, and others have said that high input costs and food inflation are hurting their business. Prices of food items, oil, coffee, and other essentials have slowed down consumption. Even company leaders admit that the middle class is under heavy pressure. Household budgets have been badly affected, and growth in the food and beverage sector has fallen sharply.

The government says inflation has come down, but shopkeepers and customers tell another story. Prices of milk, vegetables, pulses, flour, and gas are still high. For common people, inflation is not a statistic—it is the cost of daily needs that are slowly going out of reach.

At the same time, political opposition leaders have raised concerns about unemployment, rising prices, and misuse of public money. They say job opportunities are shrinking and young people are losing hope about the future.

Behind all the slogans of development, a serious problem is growing—India’s debt. In 2013–14, the country’s total debt was about ₹55 lakh crore. After more than a decade, it is close to ₹200 lakh crore. This means the current government has added much more debt in a short time compared to earlier governments.

A huge amount of money is now spent only on paying interest on loans. Foreign debt has also increased. Today, every Indian citizen carries an average debt burden of around ₹1.4 to ₹1.5 lakh.

Some states, like West Bengal, are also deeply in debt, spending a large part of their income on loan repayments. Much of the borrowing is not clearly explained to the public—where the money comes from and how it is used.

If loans were used for productive work like industries, energy, and infrastructure, they could help growth. But when debt is used for non-productive spending, it becomes dangerous. India is now at a critical point. The numbers may show growth, but people on the ground feel financial stress.

The big question is whether this growing debt can be controlled, or whether it will create a serious economic crisis in the future.

By Sarfaraz Ahmed Qasmi

Source: Haqeeqat Time